Sales for both single-family new infills and new infill townhomes cool in March, as market uncertainty starts to impact Calgary’s housing market and inventory starts to grow.

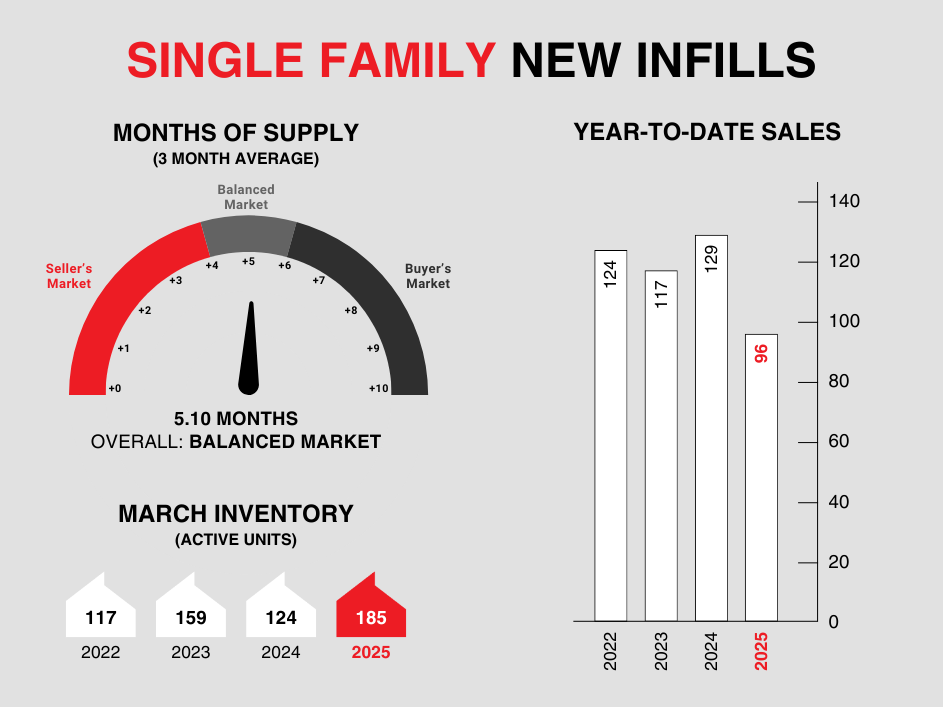

Single-family new infills posted 33 sales during March, down only slightly from the 38 sales recorded last month, but considerably lower than the 55 sales posted in March 2024. Total year-to-date sales for single-family new infills at the end of March were 96, down 26% compared to the same time in 2024; however, right on the 10-year average for Q1.

Single-family new infill inventory increased in March, up to 185 active listings from the 151 active listings recorded last month. This is an increase of 23% compared to last month and 49% compared to the same time last year.

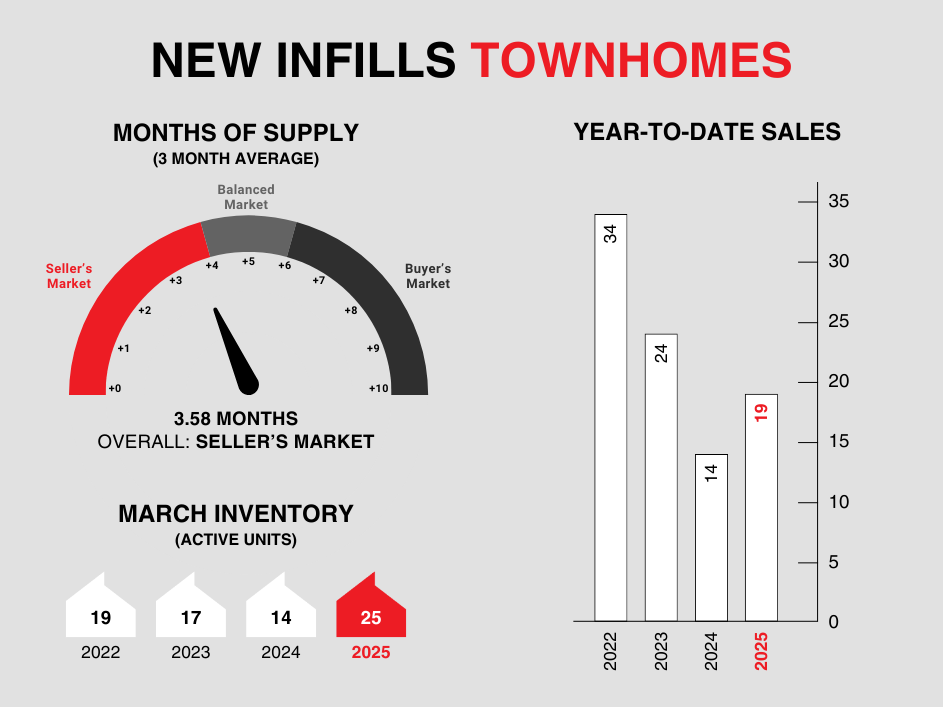

New infill townhomes posted 6 sales during March, down from the 9 sales recorded last month, but only slightly down from the 7 sales recorded in March of last year. Total year-to-date sales for new infill townhomes at the end of March were 19, which is still up 35% from last year, but down slightly from the 10-year average of 22 sales in Q1.

New infill townhome inventory rose in March, with 25 active units now for sale, up from 19 units actively listed last month. This is a considerable rise in inventory levels compared to last year, when just 14 active units were listed for sale, and the highest average Q1 inventory in 4 years.

Although March is typically one of the busiest months for real estate in Calgary, general market uncertainty due to the trade war and US tariffs has caused many home buyers to pause their searches for the time being to see how things play out. Although sales are still relatively strong and nowhere near depressed levels, cooling sales combined with rising inventories are expected to increase time on market. Depending on how many more new homes hit completion without a sale, the market may start to favour the buyer over the coming months, which could place downward pressure on prices if this continues more long-term.

On a positive note, sales prices remain strong for both single-family new infills and new infill townhomes. The average sales pricing for a new townhome in 2025 was nearly $774,603, or $459/sq ft above grade, while single-family infill sales in 2025 averaged $1,308,258 or $588 per sq ft above grade. Despite market uncertainty starting to weigh on our Spring real estate market, Calgary is still expected to fare better than our more expensive peers in Toronto and Vancouver. And, depending on what happens, pent-up demand may bring a stronger market later in the year.

CALGARY MARKET UPDATE (CREB)

City of Calgary, April 1, 2025 - Ongoing economic uncertainty, driven by tariff threats, has weighed on consumer confidence and impacted housing activity in March. Sales declined by 19 percent year-over-year, totaling 2,159 units. Sales slowed across all property types, with the steepest decline in higher-density segments.

“It is not a surprise to see a pullback in sales given the uncertainty,” said Ann-Marie Lurie, Chief Economist at CREB®. “However, it is important to note that sales remain stronger than anything reported throughout 2015 to 2020, where our economy faced significant economic challenges and job loss. Nonetheless, easing demand has been met with gains in new listings and rising inventories, helping our market shift back toward balanced conditions, following four consecutive years where the market favoured the seller.”

March reported over 4,000 new listings, causing the sales-to-new-listing ratio to drop to 54 percent, low enough to support further inventory gains. Total residential inventory levels reached 5,154 units, and the months of supply pushed up to 2.4 months. While this is a significant change from last year, with limited supply options across all property types and price ranges, conditions reflect a better balance between a seller and a buyer today. However, the market significantly varies depending on location, price point, and property type.

Improving supply has taken the pressure off home prices following the steep gains reported over the previous four years. In March, the unadjusted residential benchmark price reached $592,500, relatively stable compared to both last month and prices reported last March. Both detached and semi-detached prices remain consistent with peak prices and continue to rise, while apartment and row-style homes continue to report prices slightly lower than last year's peak.